Is THAT Gift Taxable – IRS Form 709

Is THAT Gift Taxable – IRS Form 709! The IRS instructions to Form 709 Gift Tax Return spell out the general rules for allocating the unified credit to prior gifts.

The federal government generally taxes transfers of wealth in three ways: through the estate tax, the gift tax and the generation-skipping transfer tax. Together these taxes make up what many of us refer to as the federal transfer tax system.

The gift tax is a tax on the transfer of property by one individual to another while receiving nothing, or less than full value, in return. The United States has a federal gift tax that applies to transfers of property by gift. However, there is an annual exclusion that allows you to make gifts up to a certain amount each year without having to pay gift tax.

Gift Tax can quickly reach up to 40% of the fair market value of the gift(s) given.

For tax year 2023, the annual exclusion is $17,000 per recipient. This means that you can make gifts of up to $17,000 to each recipient in a given year without having to pay gift tax or report the gift to the Internal Revenue Service (IRS). If you make gifts that exceed the annual exclusion amount, you will need to file a gift tax return (Form 709) and may owe gift tax.

Additionally, there is a lifetime exemption that allows you to make gifts up to a certain amount during your lifetime without having to pay gift tax. For tax year 2023, the lifetime exemption is $12.92 million.

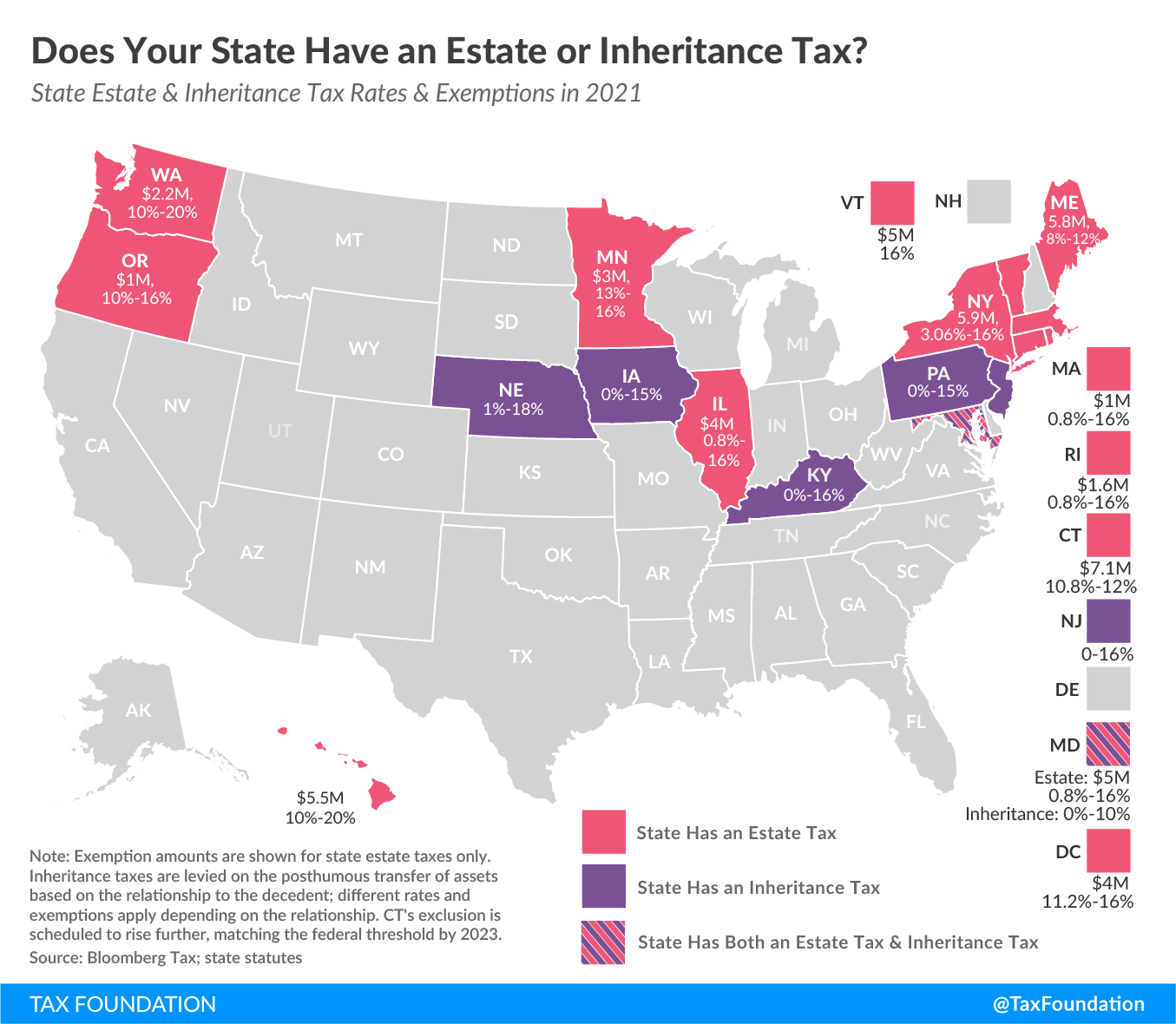

Many U.S. states ALSO impose estate and/or inheritance taxes. This post addresses federal implications with these soundbite quips:

{kind=link}

- If you give someone money or property during your life, you may be subject to the federal gift tax.

- Unless specifically excluded most gifts are subject to the gift tax.

- If you make a gift to someone else, the gift tax usually does not apply until the value of the gifts you give that person exceeds the annual exclusion for the year.

- Gift tax returns (IRS Form 709) do not need to be filed unless you give someone, other than your spouse, money or property worth more than the annual exclusion for that year.

- There is usually no tax if you make a gift to your spouse or to a charity or to pay the medical bills of another.

Who Pays the Gift Tax

The donor is generally responsible for paying the gift tax. Under special arrangements the doneemayagree to pay the tax instead. Please visit with your tax professional if you are considering this type of arrangement.

What is considered a gift

Any transfer to an individual, either directly or indirectly, where full consideration (measured in money or money’s worth) is not received in return.

What is NOT a taxable gift

The general rule is that any gift is a taxable gift. However, there are many exceptions to this rule. Generally, the following gifts are not taxable gifts.

- Gifts that are not more than the annual exclusion for the calendar year.

- Tuition or medical expenses you pay for someone (the educational and medical exclusions).

- Gifts to your spouse.

- Gifts to a political organization for its use.

In addition to this, gifts to qualifying charities are deductible from the value of the gift(s) made.

Are gifts deductible

Making a gift or leaving your estate to your heirs does not ordinarily affect your federal income tax. You cannot deduct the value of gifts you make (other than gifts that are deductible charitable contributions). If you are not sure whether the gift tax or the estate tax applies to your situation, refer to Publication 559, Survivors, Executors, and Administrators.

What other information must be filed with IRS Form 709

Refer to Form 709,709 Instructions and Publication 559. Among other items listed:

- Copies of appraisals.

- Copies of relevant documents regarding the transfer.

- Documentation of any unusual items shown on the return (partially-gifted assets, other items relevant to the transfer(s)).

How is a gift’s Fair Market Value (FMV) Determined

- Fair Market Value is defined as: “The fair market value is the price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable knowledge of relevant facts.

- The fair market value of a particular item of property includible in the decedent’s gross estate is not to be determined by a forced sale price.

- Nor is the fair market value of an item of property to be determined by the sale price of the item in a market other than that in which such item is most commonly sold to the public, taking into account the location of the item wherever appropriate.” Regulation §20.2031-1.

Can a married same sex donor claim the gift tax marital deduction for a spousal transfer?

- For federal tax purposes, the terms “spouse,” “husband,” and “wife” includes individuals of the same sex who were lawfully married under the laws of a state whose laws authorize the marriage of two individuals of the same sex and who remain married.

- Also, the Service will recognize a marriage of individuals of the same sex that was validly created under the laws of the state of celebration even if the married couple resides in a state that does not recognize the validity of same-sex marriages.

- However, the terms “spouse,” “husband and wife,” “husband,” and “wife” do not include individuals (whether of the opposite sex or the same sex) who have entered into a registered domestic partnership, civil union, or other similar formal relationship recognized under state law that is not denominated as a marriage under the laws of that state, and the term “marriage” does not include such formal relationships.

- Gifts to your spouse are eligible for the marital deduction.

- For further information, including the timeframes regarding filing claims or amended returns, see Revenue Ruling 2013-17.

- Frequently Asked Questions for same-sex couples

- FAQs for registered domestic partners and individuals in civil unions

- Publication 555, Community Property.

The Difference Between Estate and Gift Taxes

- Estate taxes and generation-skipping transfer taxes are paid on the contents of estates or proceeds of trusts.

- Gift taxes are paid on transfers of wealth between living persons.

The general rules

Taxable estates are reported using IRS Form 706. However, there are many exceptions to this rule identified in the instruction set

Taxable gifts are reported using IRS form 709. However hereto, there are many exceptions to this rule identified in the instruction set. The following gifts are not taxable gifts and do not require the filing of IRS form 709:

- Gifts that are not more than the annual exclusion for the year,

- Tuition or medical expenses you pay directly to a medical or educational institution for someone,

- Gifts to your spouse,

- Gifts to a political organization for its use, and

- Gifts to charities.

Gift Splitting

You and your spouse can make a gift up to $30,000 in 2021 to a third party without making a taxable gift. The gift can be considered as made one-half by you and one-half by your spouse. If you split a gift you made, you must file a gift tax return to show that you and your spouse agree to use gift splitting. You must file a Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return, even if half of the split gift is less than the annual exclusion. You must also file a gift tax return on Form 709, if any of the following apply:

- You gave gifts to at least one person (other than your spouse) that are more than the annual exclusion for the year.

- You and your spouse are splitting a gift.

- You gave someone (other than your spouse) a gift of a future interest that he or she cannot actually possess, enjoy, or receive income from until some time in the future.

- You gave your spouse an interest in property that will terminate due to a future event.

For more information see

- Publication 559. Guidance for survivors, executors and administrators. This publication is designed to help those in charge of the property (estate) of an individual who has died (decedent). It explains how to complete and file federal income tax returns and points out the responsibility to pay any taxes due. IT is not a ‘substantial authority’ but offers a good start.

- Form 706 PDF(PDF). Form to be filed on certain estates of a deceased resident or citizen. The catalog number for the instructions is 16779E. Prescribing Instructions are: IRC Sec. 6018; Regs. Sec. 20.6018-1.

- Form 706 Instructions PDF(PDF). This item is used to assist in filing Form 706. Form 706 is used by the executor of a decedent’s estate to figure the estate tax imposed by Chapter 11 of the Internal Revenue Code. Instructions include rate schedules.

- Form 8971 (PDF) – Information Regarding Beneficiaries Acquiring Property From a Decedent is filed by executors of an estate and other persons required to file Form 706 or Form 706-NA to report the final estate tax value of property distributed or to be distributed from the estate, if the estate tax return is filed after July 2015. Form 8971, along with a copy of every Schedule A, is used to report values to the IRS. One Schedule A is provided to each beneficiary receiving property from an estate.

- Form 8971 Instructions (PDF). This item is used to assist in filing Form 8971.

- Form 709 (PDF). Form 709 is used to report transfers subject to the Federal gift and certain generation-skipping transfer (GST) taxes, and to figure the tax, if any, due on those transfers.

- Form 709 Instructions (PDF), This item contains helpful information to be used by the taxpayer in preparation of Form 709, U.S. Gift Tax Return.Instructions include rate schedules.

- Form 2848 (PDF) – Declaration of Representative and POA used with respect to any tax imposed by the Internal Revenue Code (except alcohol and tobacco taxes and firearms activities).

- Form 2848 Instructions (PDF), This item contains general instructions for using and preparing Form 2848.

- Form 4421 (PDF) – Executor’s Commissions and Attorney’s Fees

- Form 4422 (PDF) Application for Certificate Discharging Property Subject to Estate Tax Lien

- Form 1041 (PDF) – US Income Tax Return for Estates and Trusts

- Form 1041 Instructions (PDF) – Instructions – US Income Tax Return for Estates and Trusts

- Schedule K-1 (PDF) – Beneficiary’s Share of Income, Deductions, Credits

- Section 7520 – Interest Rates to be used in valuing certain charitable transfers.

- Form 4768 (PDF) – Application for Extension of Time Tofile a Return and/or Pay US Estate (& Generation-Skipping Transfer) Taxes. – Remember to file the second page and to be sure to fill in the decedent’s name and social security number.

For more on Is THAT Gift Taxable – IRS Form 709 – contact me.

{kind=link}